Where science meets everyday wellness—expert analysis and actionable guidance to help you age smarter and stronger.

The Healthspan Report

Policy Risk Is a Wealthspan Checkup Signal

Social Security and Medicare are not disappearing, but the 2026 Trustees reports show why retirement plans should include policy risk, health-care costs, and flexible savings levers

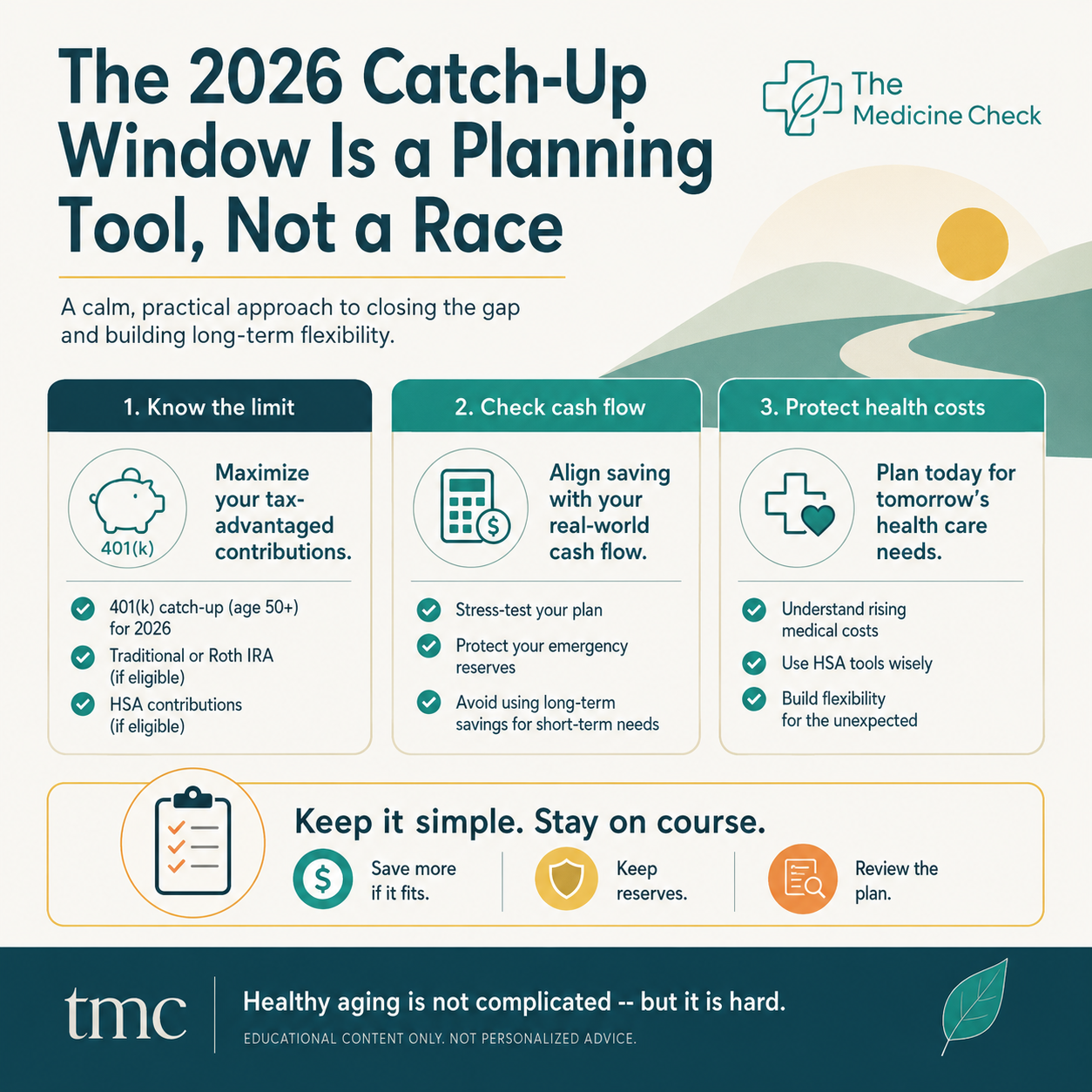

The 2026 Catch-Up Contribution Window Is a Planning Tool, Not a Race

The 2026 catch-up rules can help late-career savers, but the best Wealthspan plan balances contribution room with cash flow and healthcare-cost resilience.

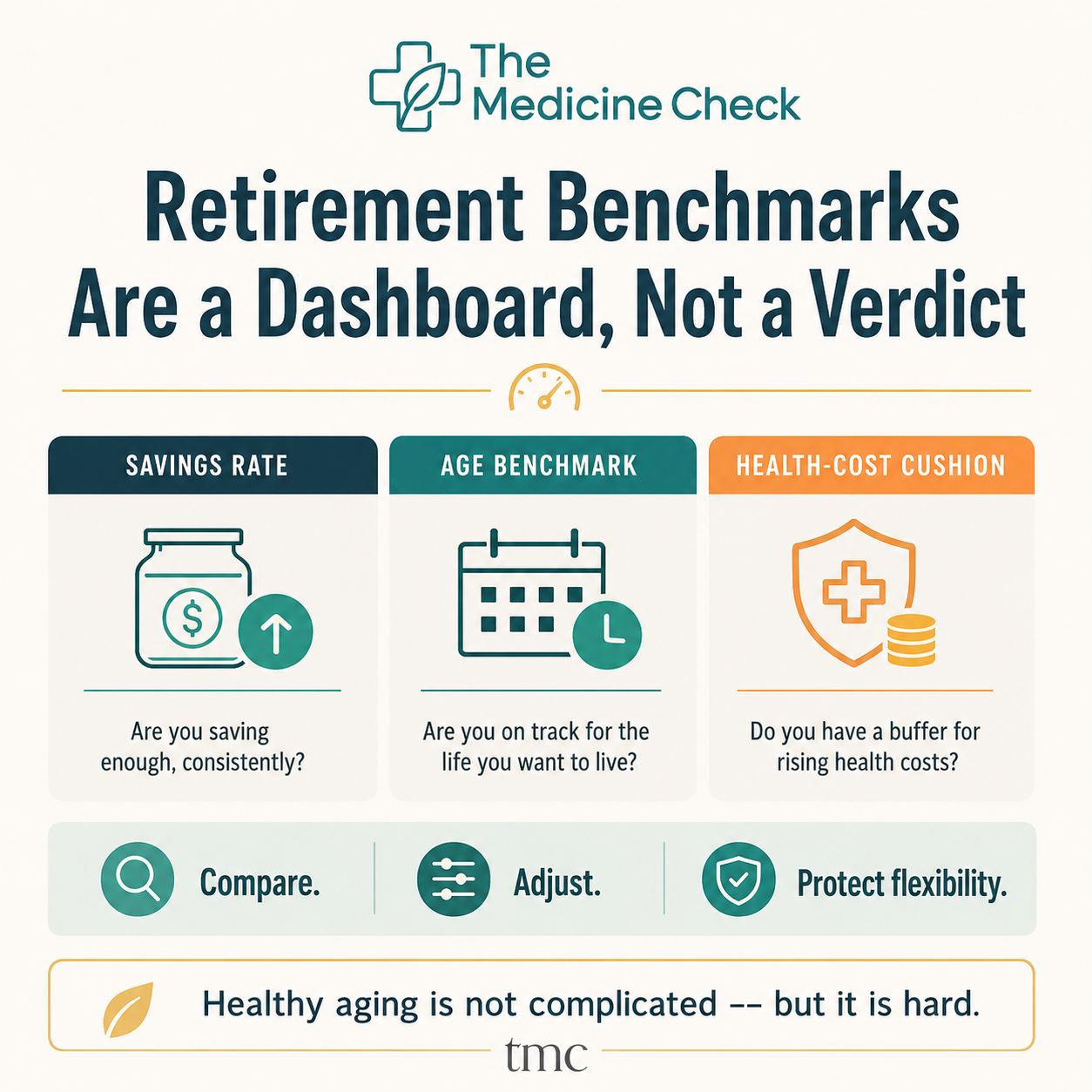

Retirement Savings Benchmarks Are a Dashboard, Not a Verdict

New Fidelity retirement data show why account balances, savings rates, age benchmarks, and health-cost planning should be read together.

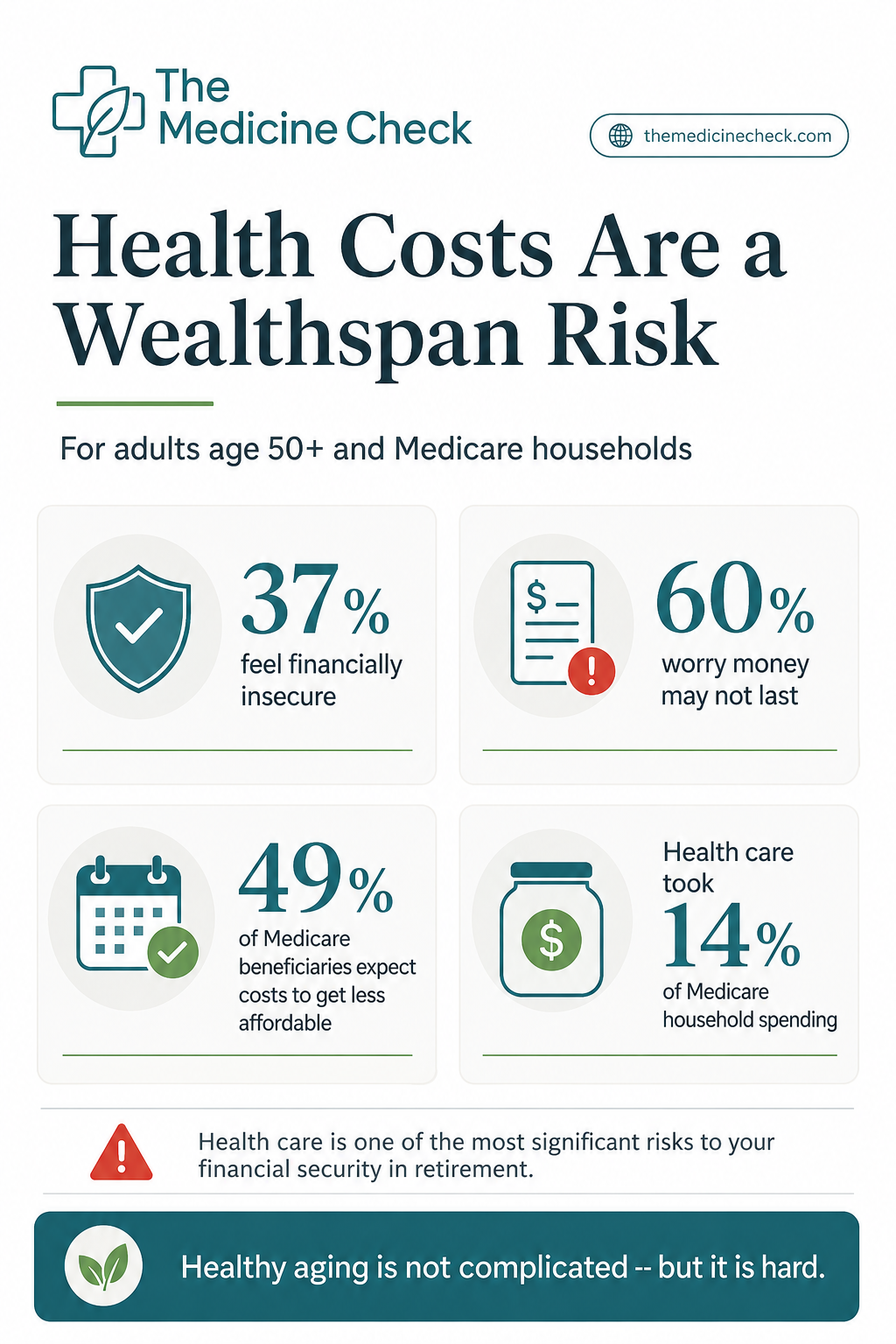

Health Costs Are Becoming a Wealthspan Risk

Health costs are not only a medical issue. New data show why they belong in every serious Wealthspan plan.

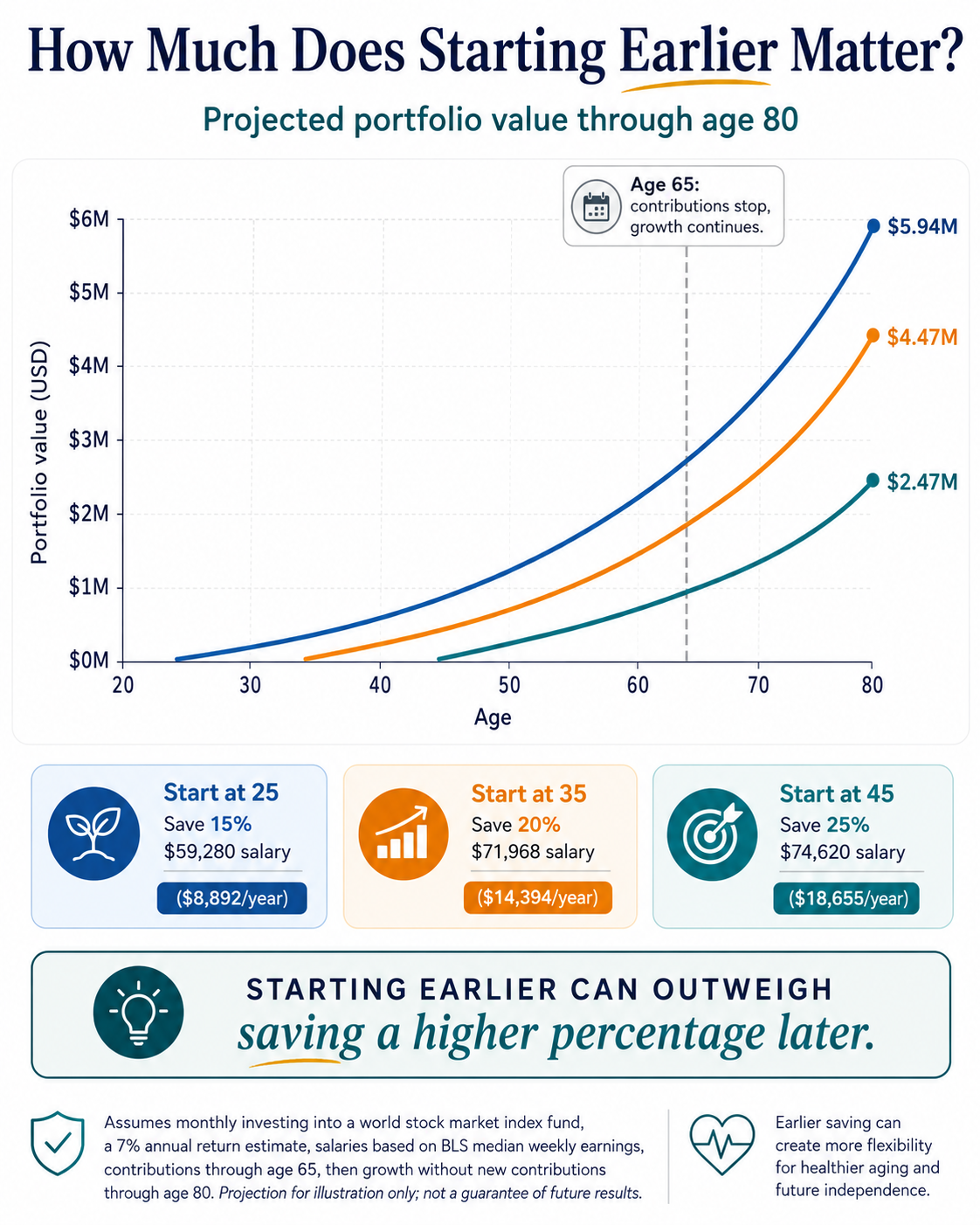

How Much Should You Really Be Saving for Retirement?

How much should you really be saving for retirement?

The common advice is to save 15% of your income, but the right number depends on when you start, how long you invest, and the kind of life you want to build. Using median U.S. salary data and a projected world stock market return, this post compares three savers who start in their 20s, 30s, and 40s.

The takeaway is clear: starting earlier can outweigh saving a higher percentage later.

But retirement planning isn’t only about maximizing your account balance. It’s about building both your wealthspan and your healthspan—so your money supports the life you want now and in the future.

The Financial Side of Illness Nobody Talks About

When illness happens, the financial impact often begins before the first bill arrives. From understanding insurance terms like deductibles and out-of-pocket maximums to navigating real-world costs and uncertainty, this experience highlights how preparation—and clarity—can make a meaningful difference when it matters most.