Where science meets everyday wellness—expert analysis and actionable guidance to help you age smarter and stronger.

The Healthspan Report

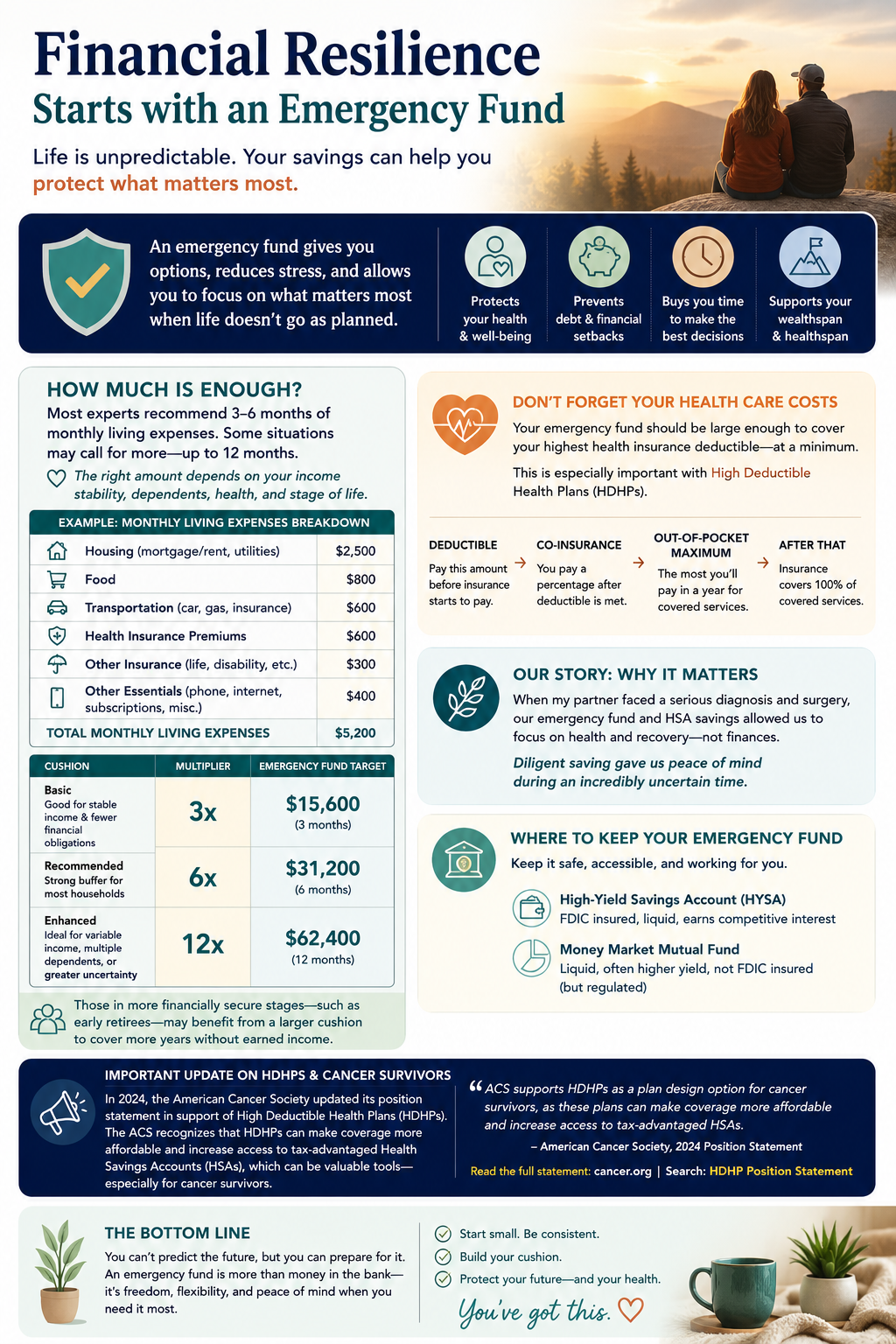

Emergency Funds: How Much Is Enough? Do You Always Need to Rebuild It Immediately?

Emergency funds are often discussed as simple financial tools: save three to six months of expenses, use it only for emergencies, and rebuild it immediately if you ever need to tap into it.

But real life is often more nuanced.

After my partner’s recent diagnosis and surgery, we used both our emergency fund and our HSA exactly as intended. What surprised me most wasn’t using the savings—it was how differently I thought about rebuilding them afterward.

This experience changed the way I think about financial security, flexibility, and the relationship between wealthspan and healthspan. Because emergency funds don’t just protect your finances. They can also protect your peace of mind, your relationships, and your ability to focus on what matters most during uncertain seasons of life.

Sometimes the greatest value of an emergency fund isn’t what it earns—but the flexibility and perspective it provides when life becomes unpredictable.

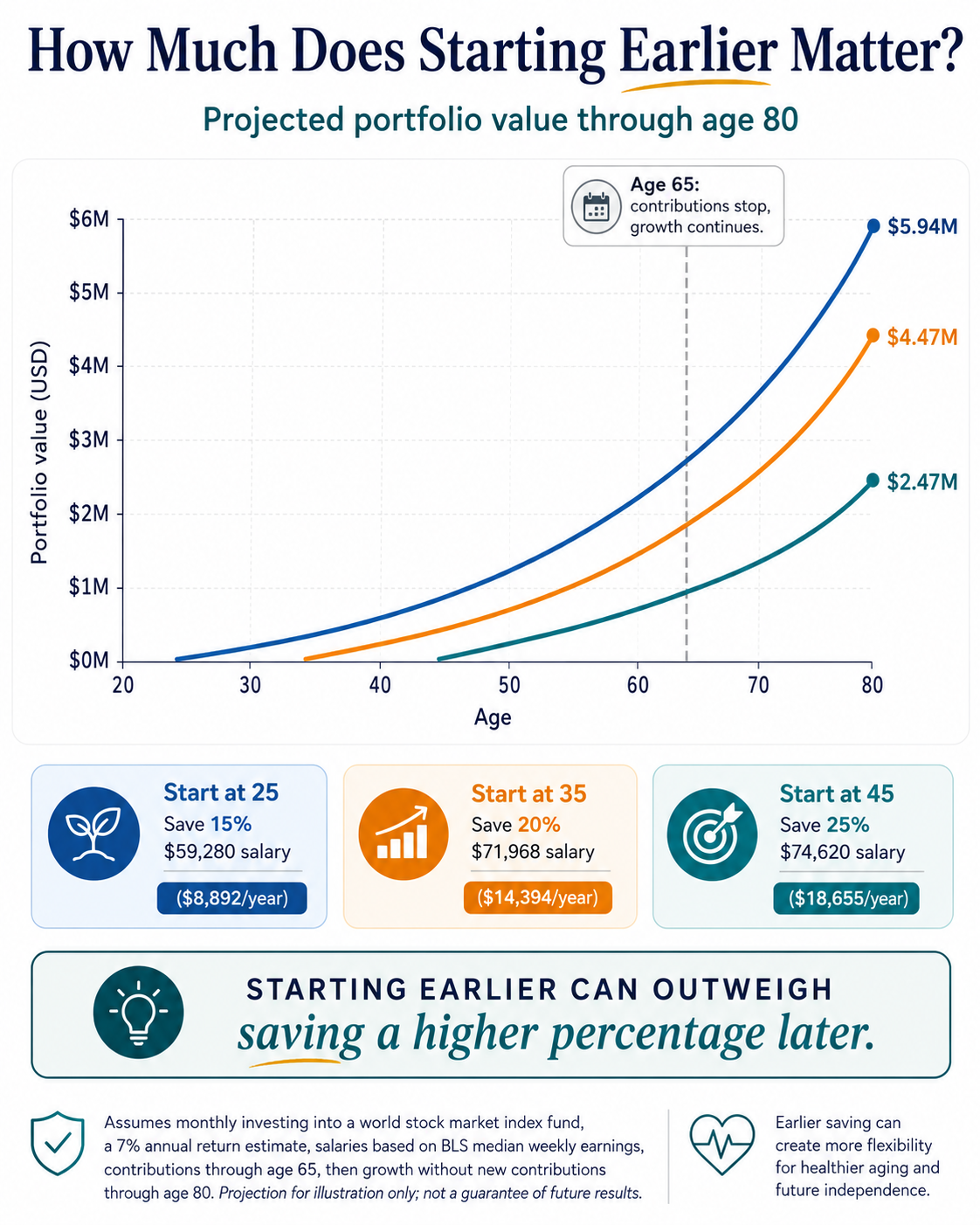

How Much Should You Really Be Saving for Retirement?

How much should you really be saving for retirement?

The common advice is to save 15% of your income, but the right number depends on when you start, how long you invest, and the kind of life you want to build. Using median U.S. salary data and a projected world stock market return, this post compares three savers who start in their 20s, 30s, and 40s.

The takeaway is clear: starting earlier can outweigh saving a higher percentage later.

But retirement planning isn’t only about maximizing your account balance. It’s about building both your wealthspan and your healthspan—so your money supports the life you want now and in the future.