How Much Should You Really Be Saving for Retirement?

“Save for retirement.” Most people know they should be doing it. Far fewer know how much is actually enough. One of the most common rules of thumb is to save 15% of your income for retirement, especially if you start early and invest consistently. Fidelity has long recommended a target savings rate of around 15%, including employer match contributions.

But in practice, the right number depends on far more than a percentage.

It depends on when you start.

It depends on the lifestyle you want.

And increasingly, it depends on the balance between your wealthspan and your healthspan.

Because retirement planning isn’t just about building the biggest possible account balance. It’s about building a life that is financially secure while still allowing you to live meaningfully along the way.

The Numbers: How Americans Are Actually Doing

Retirement savings statistics can be both encouraging and sobering.

According to Fidelity data, the average 401(k) balance in 2025 reached approximately $146,000. But averages can be misleading because they’re heavily influenced by high earners and long-term savers.

When broken down by generation, the numbers look something like this:

Millennials: around $67,000 saved

Generation X: around $192,000 saved

Baby Boomers: around $250,000 saved

For many people, these numbers feel either discouragingly low or impossibly high, but comparison is rarely useful without context.

Someone who began investing in their twenties has a dramatically different trajectory than someone who started in their forties. A physician who delayed earnings because of training may save aggressively later. A family prioritizing caregiving or health challenges may have entirely different financial realities. This is why retirement planning should never be reduced to a single benchmark.

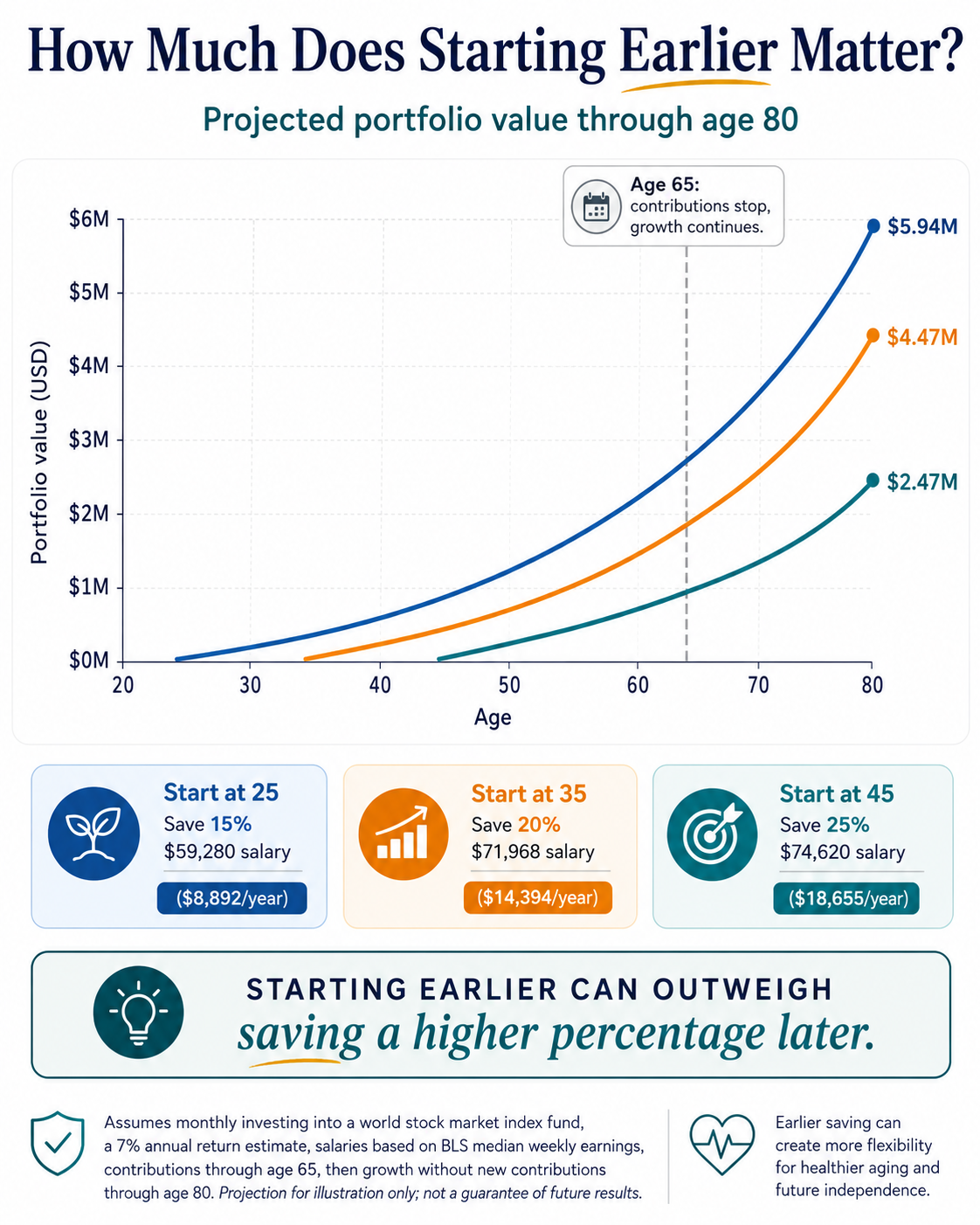

The Power of Starting Early

What matters most is often not perfection, but time and discipline

A person who consistently invests moderate amounts starting in their twenties will often outpace someone trying to “catch up” later with much larger contributions. Compound growth remains one of the most powerful forces in personal finance.

This is also why automation matters so much. When retirement contributions happen automatically, financial progress becomes less dependent on motivation or market timing. You remove decision fatigue. You prioritize your future self before lifestyle inflation quietly consumes every raise.

That principle—paying yourself first—is still one of the best financial habits you can build.

Graphic showing the difference in expected returns based on starting saving and investing earlier (age 25 vs 35 vs 45).

But There’s Another Side to the Equation

Over the past few months, I’ve written about how my partner’s health journey shifted my perspective on money and time. We still save aggressively. We still invest consistently. Our long-term financial goals haven’t disappeared.

But experiences like illness also force you to confront a difficult reality:

There is no guarantee that perfect health arrives alongside retirement.

As a geriatric physician, I see this tension often. People spend decades postponing experiences, rest, relationships, and joy in the name of someday. Then health changes. Mobility changes. Energy changes. Time changes. I am guilty of this.

That doesn’t mean retirement savings are unimportant. It means retirement planning should exist alongside living. This is where the idea of wealthspan and healthspan become deeply connected.

A large retirement account means little if your health prevents you from enjoying the life you spent decades preparing for.

So… How Much Should You Save?

For many people, aiming for 20–25% of gross income is a strong target, especially for those pursuing earlier financial independence or starting retirement savings later in life.

But the goal isn’t simply maximizing savings at all costs. The goal is balance. Save enough that your future self is protected. But don’t become so focused on tomorrow that you forget to live today.

That may mean:

Continuing automated retirement contributions

Building emergency savings

Investing consistently

While also:

Traveling with people you love

Prioritizing experiences

Improving your daily quality of life

Protecting your health now, not just later

A Better Question

Maybe the better question isn’t:

“How much should I save for retirement?”

Maybe it’s:

“How can I use money to support both my future life and my current one?”

Because financial wellness is not just about accumulating wealth. It’s about creating the freedom to live well across the entire span of your life.