The 2026 Catch-Up Contribution Window Is a Planning Tool, Not a Race

The 2026 catch-up rules create more room for late-career retirement saving, but bigger limits only help if they fit the whole Wealthspan plan.

The late-career savings window is real, but it is not magic

For many people in their 50s and early 60s, retirement planning starts to feel more concrete. The timeline is shorter. Healthcare costs feel less theoretical. Parents may need support and adult children may still need help. Work may be rewarding, tiring, uncertain, or some combination of the three. That is why the 2026 catch-up contribution rules are worth a practical Wealthspan look this week. They create more room for late-career saving, but they do not erase the need for cash flow, health-cost planning, and flexibility.

The headline number is simple: the IRS lists the 2026 elective deferral limit for traditional and safe harbor 401(k) plans at $24,500. If a plan permits catch-up contributions, participants age 50 or older may add $8,000. For employees age 60 through 63 in eligible plans, the higher catch-up contribution limit is $11,250. Those limits can be useful, but they are not a command. A strong Wealthspan plan does not chase the maximum contribution if doing so leaves the rest of life fragile.

What changed for 2026

The basic catch-up idea is straightforward. Once workers reach certain ages, tax rules may allow them to contribute more to retirement accounts than younger workers can. In 2026, Fidelity's catch-up contribution guidance summarizes several important figures: the base 401(k), 403(b), and similar workplace plan limit is $24,500; the standard age 50+ catch-up is $8,000; and the age 60 to 63 super catch-up can bring the employee contribution limit to $35,750 when a plan offers it.

Fidelity also notes an important Roth catch-up change for higher earners beginning in 2026: if a worker earned at least $150,000 in 2025, age 50+ catch-up contributions generally need to be made as Roth contributions in after-tax dollars. That does not make Roth better or worse for everyone. It means the tax treatment may be different, and affected workers should understand their plan's rules before assuming catch-up dollars work the same way they did before.

For IRAs, Fidelity lists a 2026 contribution limit of $7,500, with a $1,100 catch-up for people age 50 or older, bringing the total to $8,600. Eligibility and deductibility can depend on income, workplace plan coverage, and tax details. This is general education, not tax advice. The useful move is to know which rules might apply before the year is almost over.

Why this belongs in a Wealthspan plan

Catch-up contributions are often framed as a race to the largest possible number. Wealthspan needs a wider frame. Wealthspan is the financial capacity to age well. That means savings matter, but so do healthcare affordability, debt, cash reserves, insurance choices, work flexibility, housing, caregiving, and the ability to keep making healthy choices when life gets expensive.

EBRI's 2026 Retirement Confidence Survey shows why this wider view matters. The survey found that retirement confidence declined among both workers and retirees. Nearly 6 in 10 workers said healthcare costs were hurting their ability to save for retirement, and 2 in 5 retirees said healthcare expenses in retirement had been higher than expected.

KFF's recent Medicare affordability brief adds the older-adult context. KFF reported that Medicare beneficiaries spent an average of $6,459 out of pocket on healthcare costs in 2023, including premiums and services. KFF also noted that one in four Medicare beneficiaries had income below $24,600 per person in 2024, and that Medicare Part B premiums and deductibles are projected to rise substantially between 2026 and 2034. So the catch-up question is not only, "Can I put more into a retirement account?" It is also, "Can I do that while preserving the flexibility that protects independence?"

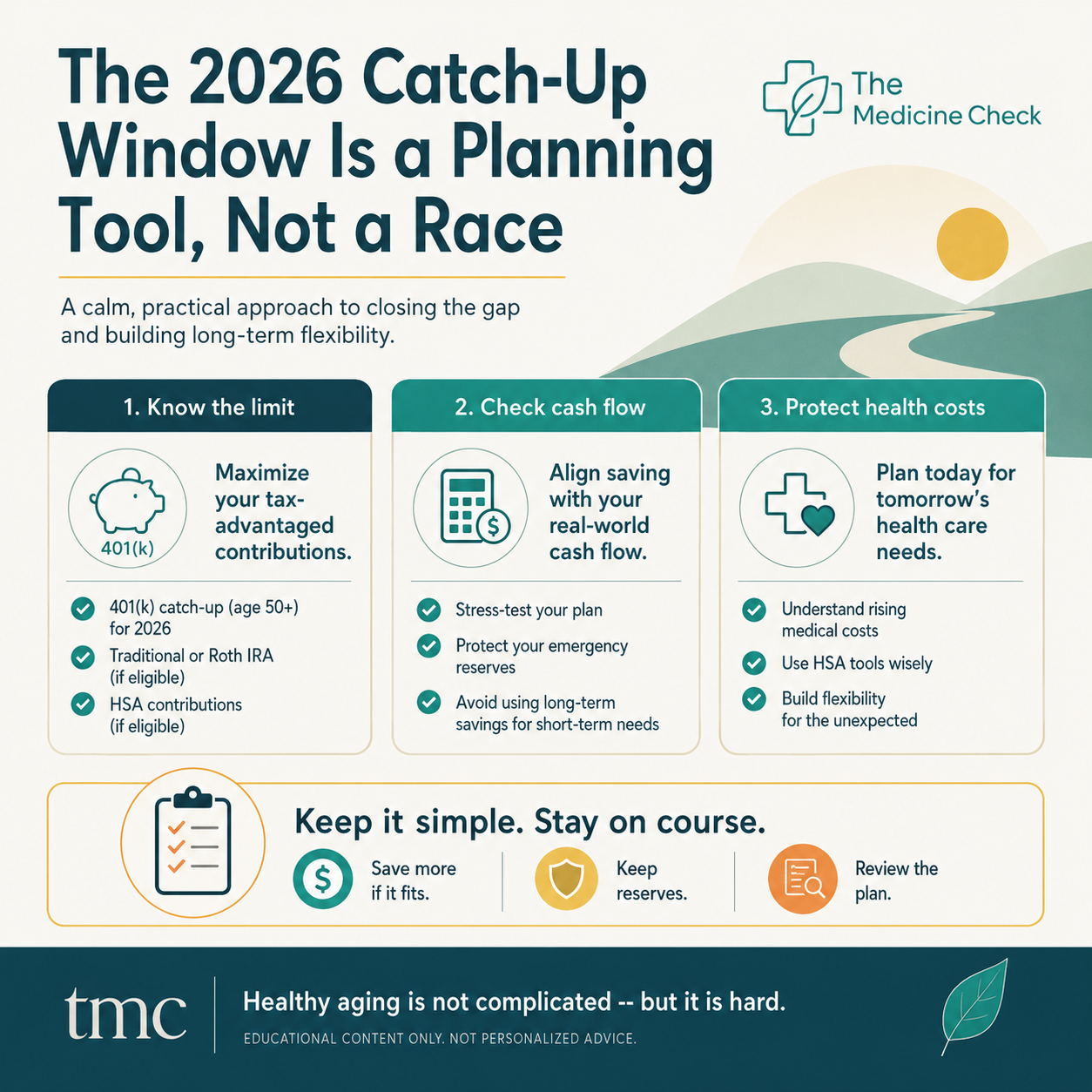

A practical catch-up review starts with three buckets:

First, know the available room. Check your plan's 2026 limits, whether catch-up contributions are offered, whether the age 60 to 63 higher catch-up applies, and whether any Roth catch-up requirement affects the account.

Second, check your household's cash flow. Increasing contributions can be powerful, but not if it forces high-interest debt, drains emergency savings, or makes routine healthcare harder to afford. A contribution rate that looks impressive on paper can still be fragile if it leaves no room for real life.

Third, protect your health-cost cushion. Late-career savers are often close enough to Medicare, retirement, or semi-retirement that healthcare costs deserve their own line in the plan. Premiums, prescriptions, dental care, vision care, hearing care, physical therapy, and caregiving can all affect whether savings translate into actual independence.

This is where The Medicine Check Annual Wealthspan + Healthspan Checkup Tracker can be useful: it gives you a way to review savings, health markers, medications, prevention habits, and planning priorities in one annual rhythm.

Before raising contributions, a household can ask four practical questions:

1. What contribution rate is already happening automatically, including any employer match?

2. Would a higher contribution still leave enough cash for emergency reserves, known healthcare costs, and debt obligations?

3. If I am age 50+ or age 60 to 63, and catch-up rules apply, does the plan actually permit those contributions?

4. If a Roth catch-up rule applies, how would after-tax contributions affect take-home pay and tax planning?

The answer does not have to be all or nothing. Some people may increase their contributions now. Some may wait until their debt is lower. Some may split the difference by raising the rate gradually. Some may decide that preserving cash for health costs, caregiving, or job uncertainty is the more resilient move this year.

Evidence verdict

The evidence is strong for the factual claim that 2026 contribution and catch-up limits create additional saving room for eligible workers. The IRS and Fidelity are appropriate sources for the limits and high-level rule changes. The evidence is also strong enough to connect late-career retirement planning with healthcare affordability risk. EBRI's survey data show that healthcare costs are already affecting workers' ability to save and retirees' expectations. KFF's Medicare analysis shows that out-of-pocket healthcare costs remain meaningful even after Medicare eligibility.

The limits are important too. None of these sources can tell one household exactly how much to contribute, whether Roth treatment is better, or which retirement account strategy is optimal. The responsible takeaway is educational: understand the rules, compare them with cash-flow reality, and avoid treating the maximum contribution as a universal target.

The bottom line

The 2026 catch-up contribution window is a tool. It can help late-career savers build more retirement flexibility. But it should be used inside a broader Wealthspan plan, not as a race against an abstract limit. The better question is not, "Can I max everything out?" It is, "Can I strengthen retirement readiness while preserving the cash, healthcare access, and flexibility that help me age well?

Healthy aging is not complicated -- but it is hard. The same is true of financial resilience. The power is in reviewing the numbers before they become urgent.

Keep Building Your Wealthspan

- Estimate future medical costs with the Retirement Healthcare Spend Estimator.

- Model savings decisions with the Retirement Savings Calculator.

- Track both money and health trends in the Annual Wealthspan + Healthspan Checkup Tracker.

Sources

Internal Revenue Service. Retirement topics - 401(k) and profit-sharing plan contribution limits. Accessed June 7, 2026. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-401k-and-profit-sharing-plan-contribution-limits

Fidelity Investments. Catch-up contributions to tax-advantaged accounts. Accessed June 7, 2026. https://www.fidelity.com/viewpoints/retirement/catch-up-contributions

Fidelity Investments. Q1 2026 Retirement Analysis. Released May 28, 2026. https://about.fidelity.com/data-and-insights/q1-2026-retirement-analysis

Employee Benefit Research Institute and Greenwald Research. 2026 Retirement Confidence Survey Finds Americans Less Confident About Retirement as Worries Grow Over Social Security, Medicare and Rising Costs. Published May 2026. https://www.ebri.org/publications/research-publications/center-publications/content/summary/2026-retirement-confidence-survey-finds-americans-less-confident-about-retirement-as-worries-grow-over-social-security--medicare-and-rising-costs

KFF. Key Facts About Health Care Affordability for People With Medicare. Published May 2026. https://www.kff.org/medicare/key-facts-about-health-care-affordability-for-people-with-medicare/