Every Job Change Is a Wealthspan Check-in

New EBRI research shows that changing jobs can change retirement-plan access. Use the moment to protect savings momentum, benefits decisions, and future flexibility.

A job change can reshape your retirement plan

Most people think about a job change in terms of salary, commute, remote work, title, culture, or career growth. But a job change can also reset parts of your Wealthspan: whether you have access to a retirement plan, how quickly you can contribute, whether you receive an employer match, what happens to an old 401(k), and how your health benefits fit your long-term plan.

That is why new research from the Employee Benefit Research Institute, published June 25, 2026, is worth treating as more than a workplace-benefits update. EBRI found that younger workers still change jobs often, but compared with an earlier generation, they were more likely to be eligible for an employer-sponsored retirement plan after a job change. The good news is that retirement-plan access appears to be improving for many workers. The caution is that every transition still creates a moment when savings momentum can be gained or lost.

This is the practical point: retirement readiness is not built only during annual reviews or milestone birthdays. It is also built during ordinary transitions, especially the moments when a paycheck, benefit package, health plan, and savings habit all change at once.

What the new EBRI research found

The EBRI issue brief compared two groups: Americans born between 1980 and 1984, using the National Longitudinal Survey of Youth 1997 panel, and an earlier cohort born between 1957 and 1964. The goal was to understand how job changes affected eligibility for employer-sponsored retirement plans over time.

The headline finding is both encouraging and sobering. By their early 40s, both groups had held more than 10 jobs on average. More than 30% of participants in both groups either gained or lost retirement-plan eligibility when switching jobs. Among the younger cohort, more than 85% had been eligible for a retirement plan by ages 39 and 40, compared with more than 75% in the earlier cohort.

Eligibility was not evenly distributed. EBRI reported that people with above-median income and tenure were eligible for a plan for more than twice as many consecutive years, on average, as those with below-median income and tenure. Education also mattered: participants with an associate degree or higher were eligible for about 1.5 times as many consecutive years as those with a high school diploma or less.

In plain English, access has improved, but the ability to stay continuously connected to a retirement plan still varies by income, tenure, education, and job stability. That makes job transitions especially important for people whose careers include contract work, layoffs, caregiving interruptions, part-time work, or frequent moves between employers.

Why is this important?

Wealthspan is the financial capacity to age with options, independence, and resilience. Retirement accounts are not the whole story, but they are one of the major tools that can preserve future flexibility.

Fidelity’s latest retirement analysis, released May 28, 2026, found that total 401(k) savings rates reached 14.4% in the first quarter of 2026, which is close to Fidelity’s suggested combined savings rate of 15%. Fidelity also reported that nearly one in five participants increased their savings rate during the quarter, in large part because of automatic increases.

Those numbers are encouraging, but they can also hide the risk of interruption. A person may leave a plan with strong auto-enrollment, auto-escalation, and matching features, then move to a plan with different rules or a waiting period. Another person may leave an old balance behind, cash out a small account, or forget to restart contributions after the first few paychecks. None of those choices is dramatic in the moment, but over decades, they will compound.

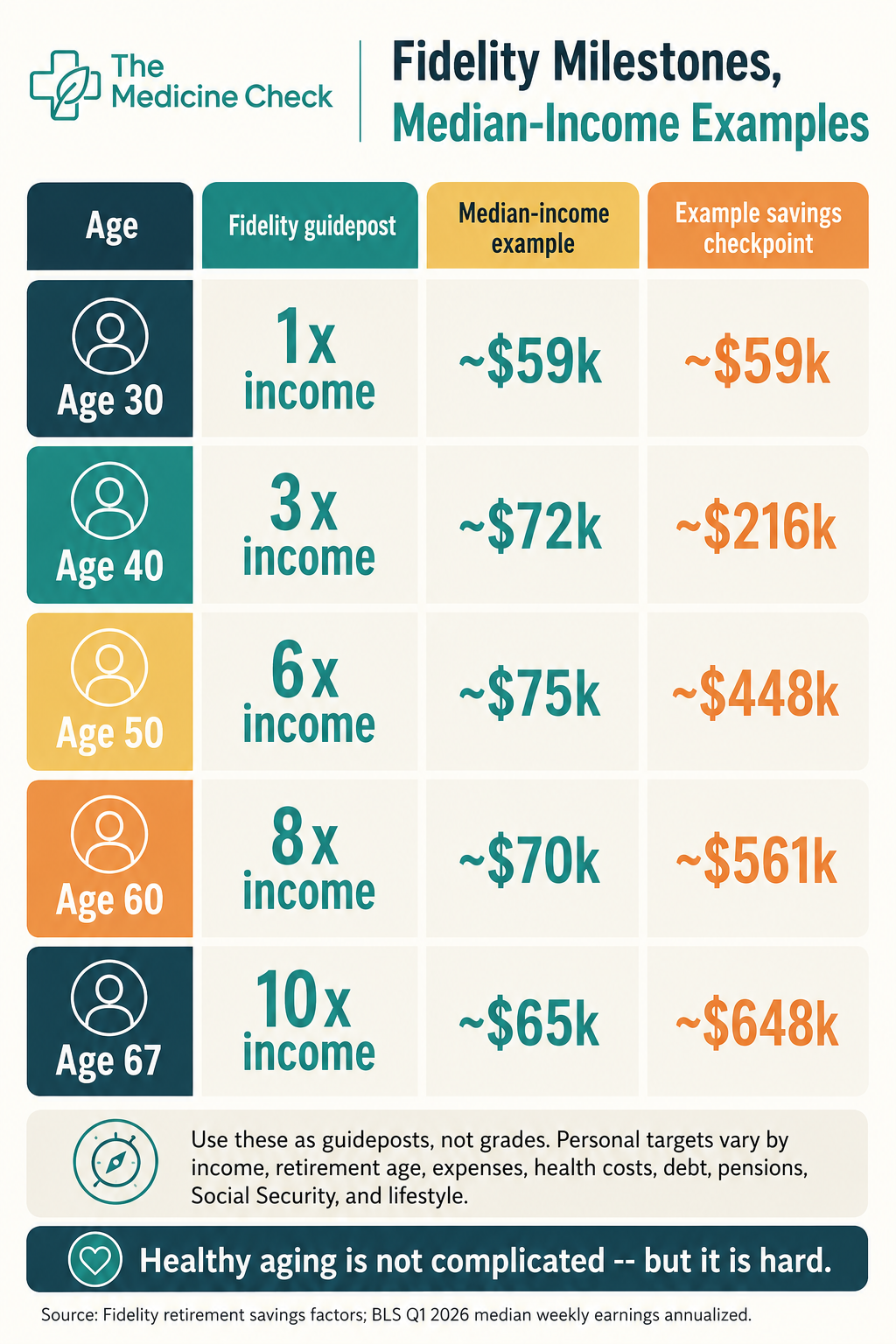

This is also where retirement savings benchmarks can help, if used gently. Fidelity’s age-based guide suggests aspirational milestones such as 1x salary by age 30, 3x by 40, 6x by 50, 8x by 60, and 10x by 67. Those are not personal grades. They are checkpoints. A job change is a natural time to ask whether the next phase of work is helping or hurting the path toward long-term independence.

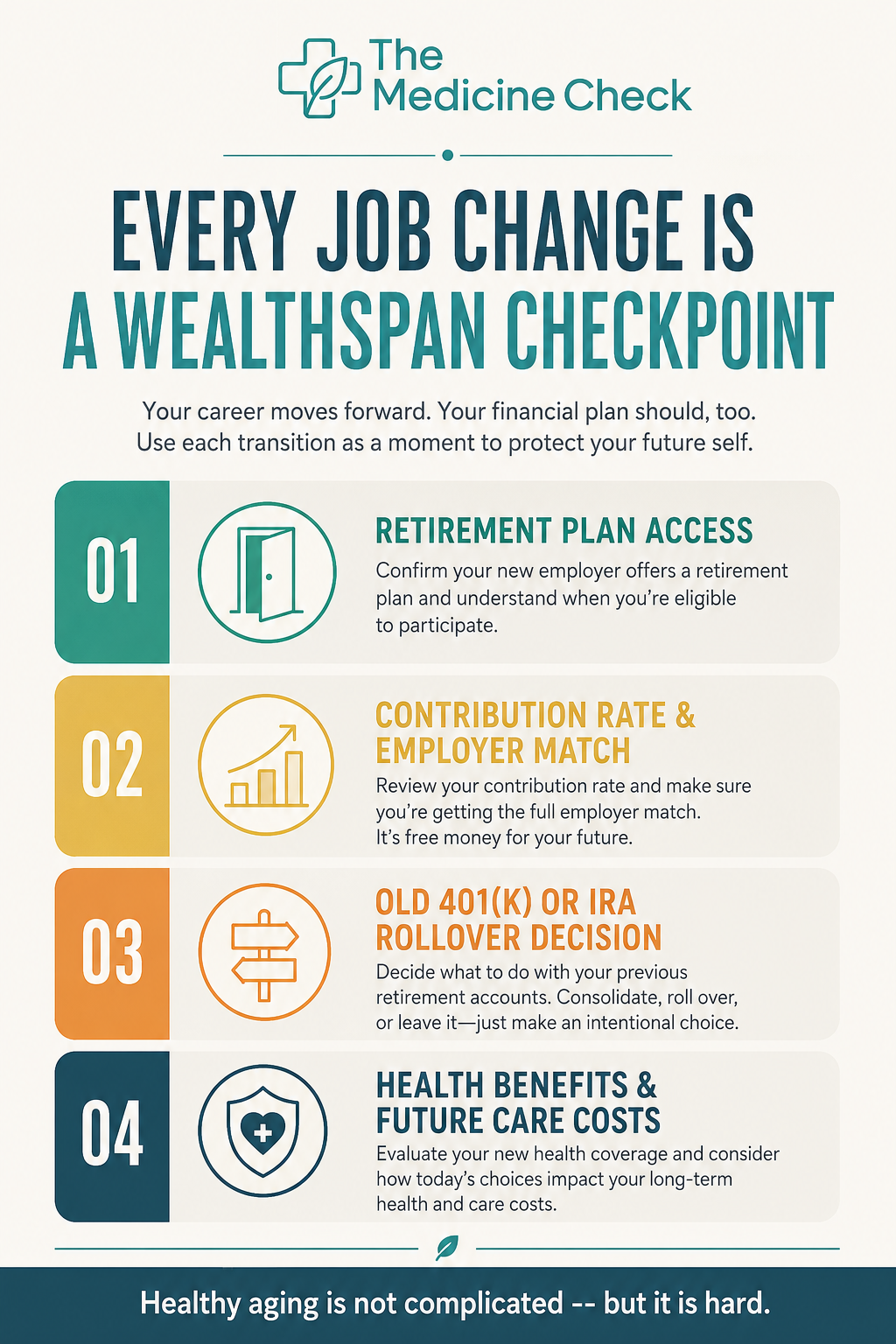

The four-point job-change Wealthspan checkup

Retirement plan access: Ask when you become eligible for the new plan, whether automatic enrollment applies, what the default contribution rate is, and how the employer match works. If there is a waiting period, note when the first contribution can start.

Contribution rate and match: Compare your old contribution rate with the new one. A raise, bonus, or new salary can be a chance to revisit the percentage, but the right number depends on cash flow, debt, emergency savings, taxes, and household priorities.

Old account decisions: Know where your old 401(k), 403(b), or similar plan will live. Some people keep an old employer plan, roll assets to a new plan, roll to an IRA, or use another appropriate path. Each option can involve fees, investment choices, creditor protections, tax rules, and administrative tradeoffs.

Health benefits and future care costs: Compare premiums, deductibles, provider networks, prescription coverage, HSA eligibility, and out-of-pocket exposure. Healthcare affordability is part of Wealthspan because future independence depends partly on being able to access care, medications, prevention, and follow-up without destabilizing the rest of the plan.

Do not let the benchmark become the whole story

The most tempting mistake is to reduce retirement readiness to one account balance. Fidelity’s average 401(k) balance data can be useful for context, but averages are shaped by income, age, tenure, market returns, account consolidation, and whether someone has savings outside a workplace plan. A person with a lower 401(k) balance may have a pension, home equity, brokerage savings, an HSA, or a spouse’s plan. Another person with a higher balance may still be exposed to health costs, debt, caregiving obligations, or an early retirement caused by illness or job loss.

That is why the better question is not “Am I ahead or behind everyone else?” The better Wealthspan question is “Did this transition make my future more flexible or more fragile?”

KFF’s Medicare affordability work is a useful reminder that retirement planning does not stop with an account balance. KFF projects that Medicare Part B premiums and deductibles will rise substantially between 2026 and 2034, and it reported that half of Medicare beneficiaries age 65 and older were worried about prescription drug affordability in 2026. A plan that protects retirement savings but ignores future care costs is incomplete.

A midyear action step

If you changed jobs recently, expect to change jobs soon, or have old retirement accounts scattered across prior employers, use this as a midyear check-in.

Write down five items: current retirement-plan contribution rate, employer match rules, old account locations, health plan out-of-pocket exposure, and whether your emergency fund could absorb a benefits or medical-cost surprise. Then review whether your current setup supports the future you are trying to protect: work optionality, healthcare affordability, independence, and enough flexibility to keep making healthy choices as you age.

The bottom line

A job change is not just a career event. It is a Wealthspan event. It can improve access to retirement savings, strengthen a contribution habit, introduce a better match, or create a chance to clean up old accounts. It can also interrupt savings, complicate healthcare coverage, or make future costs easier to ignore.

The new EBRI research points to progress in retirement-plan access for younger workers, but it also shows why transitions deserve attention. Healthy aging is supported by strong habits, good care, and financial systems that keep people from becoming fragile when life changes.

Keep Building Your Wealthspan

Estimate future medical costs with the Retirement Healthcare Spend Estimator.

Model savings decisions with the Retirement Savings Calculator.

Track both money and health trends in the Annual Wealthspan + Healthspan Checkup Tracker.

-

Employee Benefit Research Institute. New EBRI Research Finds Younger Workers Are More Likely to Be Eligible for a Retirement Plan After Changing Jobs. Published June 25, 2026. https://www.ebri.org/content/new-ebri-research-finds-younger-workers-are-more-likely-to-be-eligible-for-a-retirement-plan-after-changing-jobs

Employee Benefit Research Institute. Retirement Plan Eligibility Over Time: Comparing Findings From the National Longitudinal Survey of Youth 1997 Panel and the National Longitudinal Survey of Youth 1979 Panel. Published June 18, 2026. https://www.ebri.org/content/retirement-plan-eligibility-over-time--comparing-findings-from-the-national-longitudinal-survey-of-youth-1997-panel-and-the-national-longitudinal-survey-of-youth-1979-panel

Fidelity Investments. Fidelity Q1 2026 Retirement Analysis: 401(k) and 403(b) Savings Rates Reach Record Levels, Despite Uncertain Economy. Released May 28, 2026. https://newsroom.fidelity.com/pressreleases/fidelity-q1-2026-retirement-analysis--401-k--and-403-b-savings-rates-reach-record-levels--despite-u/s/f8f4ee41-ab58-4f14-9adb-dcb4feb3f2c7

Fidelity Investments. How much do I need to retire? Accessed June 28, 2026. https://www.fidelity.com/viewpoints/retirement/how-much-do-i-need-to-retire

Fidelity Investments. How do your retirement savings stack up? Accessed June 28, 2026. https://www.fidelity.com/learning-center/personal-finance/average-retirement-savings

Internal Revenue Service. 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500. Published November 13, 2025. https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

Internal Revenue Service. Retirement topics - Catch-up contributions. Accessed June 28, 2026. https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-catch-up-contributions

KFF. Key Facts About Health Care Affordability for People With Medicare. Published May 2026. https://www.kff.org/medicare/key-facts-about-health-care-affordability-for-people-with-medicare/