Emergency Funds: How Much Is Enough? Do You Always Need to Rebuild It Immediately?

The Purpose of an Emergency Fund

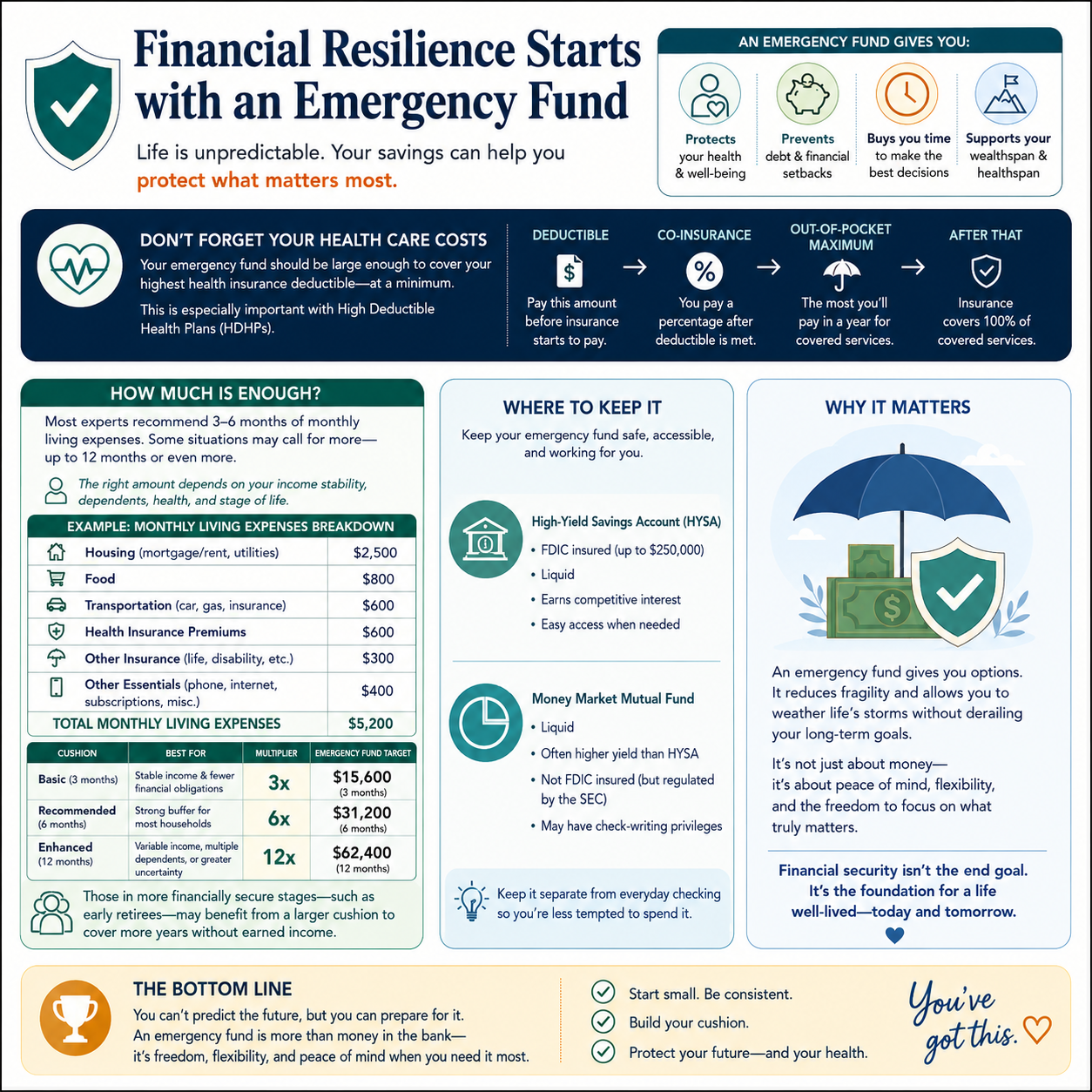

Emergency funds are one of the foundations of good financial planning. They’re practical. Predictable. Responsible. Build three to six months of expenses. Keep it somewhere safe and accessible. Use it only for true emergencies. And if you ever need to tap into it, replenish it as quickly as possible. That’s the standard advice, and in many situations, it’s great advice.

But as with most areas of life and finance, reality is often more nuanced.

Recently, my partner went through a serious diagnosis and surgery. We had an emergency fund. We had savings in our HSA. And when we needed them, we used them. In many ways, the system worked exactly as intended. What surprised me wasn’t that we used the emergency fund. That’s what it was there for. What surprised me was how differently I felt afterward.

Historically, my instinct would have been straightforward: rebuild it immediately. Replenish every dollar as quickly as possible. Return to the target balance. Restore the safety net. But this time, that urgency felt different.

The importance of an emergency fund

Emergency Funds Protect More Than Finances

Part of that shift came from recognizing what the emergency fund had actually provided during this experience. It wasn’t just money. It was flexibility. It was reduced stress. It was the ability to focus on health, recovery, and decision-making without simultaneously worrying about every unexpected expense.

That’s something we don’t talk about enough when discussing emergency savings. Emergency funds are not simply financial tools. They are health tools too. Financial stress affects sleep, mental health, relationships, and even physical well-being. During a health crisis, the emotional bandwidth required just to navigate appointments, treatment decisions, recovery, and uncertainty can already feel overwhelming. Having accessible savings creates space to breathe.

In that sense, emergency funds support both wealthspan and healthspan.

How Much Is Enough?

The traditional recommendation is often to keep three to six, and sometimes even twelve, months of expenses in cash, though the “right” amount depends heavily on your circumstances.

Someone with highly variable income may want a larger cushion. A dual-income household with stable employment may need less. A physician with consistent income and access to taxable investments may think differently about cash reserves than someone working in a more volatile industry. There’s no universally perfect number.

But there’s another question I’ve been thinking about recently: Do you always need to aggressively rebuild your emergency fund immediately after using it? I think the answer is sometimes no. That doesn’t mean abandoning financial discipline. It doesn’t mean ignoring risk. But there are seasons of life where optimization may not be the highest priority.

When Priorities Shift

In our case, we still continue to save aggressively for retirement. Our long-term financial goals haven’t changed.

But after this experience, we also became more intentional about allocating resources toward living and spending based on our values. That includes experiences that matter to us, time outdoors, travel, and creating a home environment that improves daily life. Before this, my mindset would have interpreted nearly every available dollar through the lens of future optimization. Now, I think more about balance. There is certainly wisdom in rebuilding financial resilience over time. But there is also wisdom in recognizing that money is ultimately meant to support life, not simply accumulate indefinitely.

As a geriatric physician, I see the tension between health and time constantly. Many people postpone meaningful experiences for a future they assume will arrive exactly as planned. But health changes. Mobility changes. Energy changes. Life changes. That doesn’t mean planning for the future is wrong. It means financial planning should exist alongside living.

The Real Value of Financial Security

An emergency fund is valuable because it gives you options. It reduces fragility. It allows you to weather difficult moments without destabilizing your entire life. And sometimes, after surviving one of those difficult moments, it’s reasonable to thoughtfully reassess not only your finances, but also your priorities. We are still rebuilding our savings. Just not with the same urgency I once would have felt.

Because this experience reminded me that financial security is not my ultimate goal. Money is just the tool to my goal, and the goal is creating a life supported by both financial stability and meaningful living. A healthy wealthspan will support a healthy healthspan. Discipline and savings cannot be ignored or put off indefinitely, but there is fluidity in everything that we do. The greatest value of an emergency fund is not what it earns, but the peace, flexibility, and perspective it provides when life becomes uncertain.